UPDATED : 2015-07-18

BY Edward Tse

Dr. Edward Tse believes the rise of Chinese entrepreneurship will remake the country and change the world.

Many people believe China’s economy is dominated by its state owned enterprises, which are typically large, supported by the government and enjoy preferential market access. Some call it “state capitalism”. While this perception is not entirely incorrect, it is being challenged by the rapidly developing private business sector.

Over the past two decades and more, entrepreneurship in China has grown at an exponential rate. As a result, it is bringing forth disruptive changes not only in China but increasingly on a global scale.

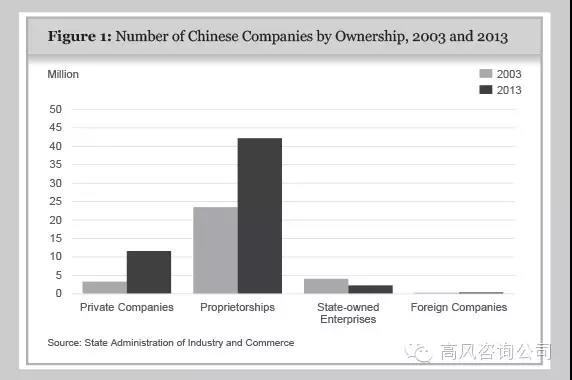

In 2000, total revenues earned by Chinese state-owned industrial companies and those in the non-state- owned sector were roughly the same, at about 4 trillion yuan (HK$5 trillion) each. By 2013, while total revenues at state-owned companies had risen just over six fold, revenues in the non-state sector had risen by more than 18 times. Profits in the same period showed an even more remarkable difference, with state-owned companies showing a seven fold increase but profits at non-state-owned ones increasing nearly 23 times.

China’s entrepreneurs will be the ones driving the nation forward in the coming decades. Moreover, the entrepreneurial spirit runs deeper than just in business. It manifests itself in the government, and in the desires of ordinary people, most of whom share the dream of seeing their country reclaim its place as one of the world’s great sources of scientific ideas and technological advances.

China has the potential to emerge as a key force indetermining the direction the world will take through the 21st century. The reason is the role its entrepreneurs have assumed in the nation’s development.Through this process, they will change the world – not because they set out to do so, but because they can’t avoid it.

Given the inter connectedness of our world and China’s enormous scale, they cannot realise their potential without changing China, and they cannot change China without changing the world. China’s entrepreneurship, shaped by the country’s history and culture, both in theshort and long term, will inevitably intermix with global entrepreneurship.

As this happens, China’s entrepreneurs will no longer be able to ignore the most pressing global problems, above all, climate change and the environmental stress generated as more people become wealthy and begin consuming more of everything. They will have to be involved in solving these problems. Because of this, thanks to its entrepreneurs, China will be a leading source of the thinking and practices needed to overcome the challenges facing the world in the coming decades.

The world is interdependent and, barring major disasters, will only become more so. The question, therefore, is how and on what terms should other countries engage with China, and vice versa. Given China’s rate of economic growth, and the fact it could overtake the US in the near future to become the world’s biggest economy, the initial reaction in much of the West is to see it as a threat.

Indeed, already, it is clear that it is difficult for many in America and Europe to view with equanimity a world in which a new power with its own agenda is emerging. The current world was shaped by ideas that came out of Europe and America in the 18th through to the 20th centuries. But, now, with the emergence of Asia and especially China as a new centre of global economic gravity, new thinking is needed.

With the West looking less confident about its position, and its leadership losing credibility in many parts of the world,there is an opportunity for revolutionary new approaches. Despite the fears about the rise of a powerful China, the rest of the world needs to consider howbest to react to this change. Othersneed to see China’s re-emergence from a broader perspective, rather thanjust an economic story. They need to see that China’s entrepreneurs are alsodriving a renaissance that will have a wide-ranging impact in a host of fields,much of which they, too, can benefit from.

A unique phenomenon is taking place in China today.While its political system is in herited from a top-down planned economy hierarchy, its leading entrepreneurial companies, especially in the internet industry, which are young and dynamic, borrow much of their mindset, cultureand structure from America’s Silicon Valley.

In fact, many are closer to Silicon Valley than Beijing. In these companies, China’s political and economic structure is mixed with Silicon Valley culture, each influencing the other.

Finally, I believe that as a consequence of theopening driven by China’s entrepreneurs, the push to invest in science,research and development, and the new freedoms that people are enjoying, China has embarked on a renaissance that could bring it back to its historic heights.

The jury is still out but it is moving in the right direction.

This time, China’s impact could extend much further– with the country playing a crucial role in shaping global well-being and even global governance.

Edward Tse is founder and CEO of Gao Feng Advisory Company, a global strategy consulting firm with roots in China. He is the author of the book, China’s Disruptors. www.chinasdisruptors.com

Used title: “China will reclaim its place at the top of global order, thanks to its new breed of entrepreneurs” on South China Morning Post Website.